Open in the MATLAB editor: d03ne_example

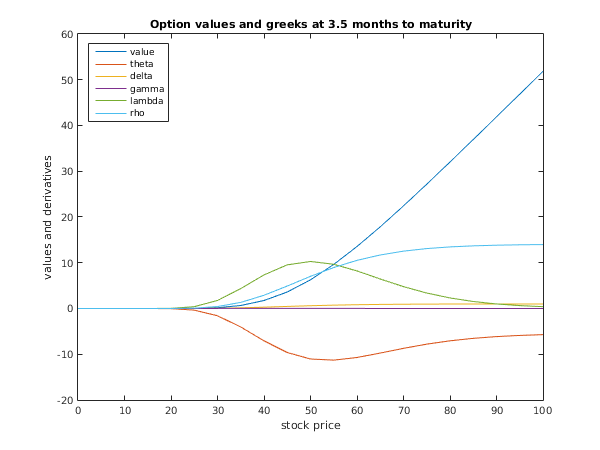

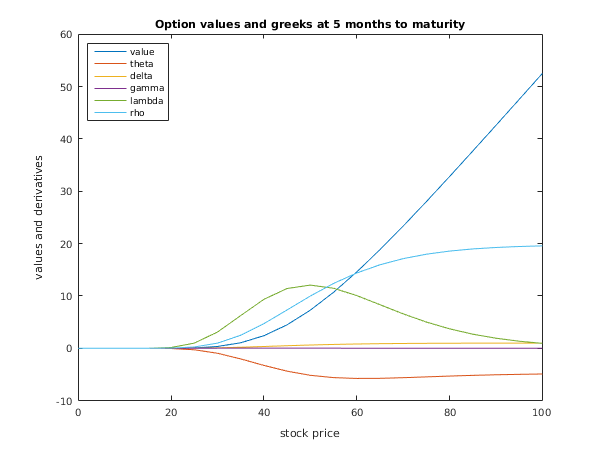

function d03ne_example fprintf('d03ne example results\n\n'); tmat = 0.4166667; td = [0:0.1:0.5]; rd = [0.1:0.01:0.15]; sigd = [0.3 0.46 0.54 0.54 0.36 0.3]; % American 5-month call option, exercise price 50 kopt = int64(2); x = 50; ns = 21; nt = 4; s_beg = 0; t_beg = 0; s_end = 100; t_end = 0.125; tmat = 0.4166667; tdpar = [true; false; true]; q = [0]; % Discretize s and t ds = (s_end-s_beg)/(ns-1); dt = (t_end-t_beg)/(nt-1); s = [s_beg:ds:s_end]; t = [t_beg:dt:t_end]; f = zeros(ns,nt); theta = f; delta = f; gamma = f; lambda = f; rho = f; % Loop over times and prices for j = 1:nt % Find average values of r and sigma [ra, ifail] = d03ne( ... t(j), tmat, td, rd); [siga, ifail] = d03ne( ... t(j), tmat, td, sigd); for i = 1:ns [f(i,j),theta(i,j),delta(i,j),gamma(i,j),lambda(i,j),rho(i,j),ifail] = ... d03nd( ... kopt, x, s(i), t(j), tmat, tdpar, ra, q, siga); end end % Tabulate option values only print_greek(ns,nt,tmat,s,t,'Option Values',f); % print_greek(ns,nt,tmat,s,t,'Theta',theta); % print_greek(ns,nt,tmat,s,t,'Delta',delta); % print_greek(ns,nt,tmat,s,t,'Gamma',gamma); % print_greek(ns,nt,tmat,s,t,'Lambda',lambda); % print_greek(ns,nt,tmat,s,t,'Rho',rho); % plot initial and final option values and greeks fig1 = figure; plot(s,f(:,1),s,theta(:,1),s,delta(:,1),s,gamma(:,1),s,lambda(:,1),s,rho(:,1)); legend('value','theta','delta','gamma','lambda','rho','Location','NorthWest'); title('Option values and greeks at 5 months to maturity'); xlabel('stock price'); ylabel('values and derivatives'); fig2 = figure; plot(s,f(:,4),s,theta(:,4),s,delta(:,4),s,gamma(:,4),s,lambda(:,4),s,rho(:,4)); legend('value','theta','delta','gamma','lambda','rho','Location','NorthWest'); title('Option values and greeks at 3.5 months to maturity'); xlabel('stock price'); ylabel('values and derivatives'); function print_greek(ns,nt,tmat,s,t,grname,greek) fprintf('\n%s\n\n',grname); fprintf(' Stock Price | Time to Maturity (months)\n'); fprintf('%16s %12.4e%12.4e%12.4e%12.4e\n', '|', 12*(tmat-t)); fprintf('%15s+%48s\n', '---------------', ... '-------------------------------------------------'); for i = 1:ns fprintf('%12.4e%4s %12.4e%12.4e%12.4e%12.4e\n', s(i), '|', greek(i,:)); end

d03ne example results

Option Values

Stock Price | Time to Maturity (months)

| 5.0000e+00 4.5000e+00 4.0000e+00 3.5000e+00

---------------+-------------------------------------------------

0.0000e+00 | 0.0000e+00 0.0000e+00 0.0000e+00 0.0000e+00

5.0000e+00 | 8.3570e-14 1.6081e-14 1.1216e-15 1.9522e-17

1.0000e+01 | 2.5775e-07 1.0991e-07 2.8081e-08 3.5715e-09

1.5000e+01 | 1.7581e-04 1.0511e-04 4.6513e-05 1.3698e-05

2.0000e+01 | 6.9193e-03 4.9696e-03 2.9591e-03 1.3701e-03

2.5000e+01 | 7.0752e-02 5.6767e-02 4.0397e-02 2.4520e-02

3.0000e+01 | 3.4255e-01 2.9499e-01 2.3506e-01 1.6927e-01

3.5000e+01 | 1.0512e+00 9.4849e-01 8.1382e-01 6.5475e-01

4.0000e+01 | 2.3997e+00 2.2341e+00 2.0134e+00 1.7424e+00

4.5000e+01 | 4.4829e+00 4.2630e+00 3.9702e+00 3.6055e+00

5.0000e+01 | 7.2786e+00 7.0226e+00 6.6859e+00 6.2677e+00

5.5000e+01 | 1.0687e+01 1.0414e+01 1.0063e+01 9.6324e+00

6.0000e+01 | 1.4580e+01 1.4305e+01 1.3959e+01 1.3546e+01

6.5000e+01 | 1.8832e+01 1.8563e+01 1.8236e+01 1.7855e+01

7.0000e+01 | 2.3337e+01 2.3079e+01 2.2774e+01 2.2429e+01

7.5000e+01 | 2.8016e+01 2.7768e+01 2.7485e+01 2.7173e+01

8.0000e+01 | 3.2809e+01 3.2573e+01 3.2308e+01 3.2022e+01

8.5000e+01 | 3.7678e+01 3.7450e+01 3.7201e+01 3.6935e+01

9.0000e+01 | 4.2595e+01 4.2374e+01 4.2136e+01 4.1885e+01

9.5000e+01 | 4.7543e+01 4.7327e+01 4.7097e+01 4.6856e+01

1.0000e+02 | 5.2510e+01 5.2298e+01 5.2074e+01 5.1840e+01