PDF version (NAG web site

, 64-bit version, 64-bit version)

NAG Toolbox: nag_tsa_cp_pelt (g13na)

Purpose

nag_tsa_cp_pelt (g13na) detects change points in a univariate time series, that is, the time points at which some feature of the data, for example the mean, changes. Change points are detected using the PELT (Pruned Exact Linear Time) algorithm using one of a provided set of cost functions.

Syntax

[

tau,

sparam,

ifail] = g13na(

ctype,

y, 'n',

n, 'beta',

beta, 'minss',

minss, 'param',

param)

[

tau,

sparam,

ifail] = nag_tsa_cp_pelt(

ctype,

y, 'n',

n, 'beta',

beta, 'minss',

minss, 'param',

param)

Description

Let denote a series of data and denote a set of ordered (strictly monotonic increasing) indices known as change points with and . For ease of notation we also define . The change points, , split the data into segments, with the th segment being of length and containing .

Given a cost function,

nag_tsa_cp_pelt (g13na) solves

where

is a penalty term used to control the number of change points. This minimization is performed using the PELT algorithm of

Killick et al. (2012). The PELT algorithm is guaranteed to return the optimal solution to

(1) if there exists a constant

such that

for all

.

nag_tsa_cp_pelt (g13na) supplies four families of cost function. Each cost function assumes that the series,

, comes from some distribution,

. The parameter space,

is subdivided into

containing those parameters allowed to differ in each segment and

those parameters treated as constant across all segments. All four cost functions can then be described in terms of the likelihood function,

and are given by:

where

is the maximum likelihood estimate of

within the

th segment. In all four cases setting

satisfies equation

(2). Four distributions are available: Normal, Gamma, Exponential and Poisson. Letting

the log-likelihoods and cost functions for the four distributions, and the available subdivisions of the parameter space are:

- Normal distribution:

- Mean changes:

- Variance changes:

- Both mean and variance change:

- Gamma distribution:

- Exponential Distribution:

- Poisson distribution:

- Mean changes:

when calculating for the Poisson distribution, the sum is calculated for rather than .

References

Chen J and Gupta A K (2010) Parametric Statistical Change Point Analysis With Applications to Genetics Medicine and Finance Second Edition Birkhäuser

Killick R, Fearnhead P and Eckely I A (2012) Optimal detection of changepoints with a linear computational cost Journal of the American Statistical Association 107:500 1590–1598

Parameters

Compulsory Input Parameters

- 1:

– int64int32nag_int scalar

-

A flag indicating the assumed distribution of the data and the type of change point being looked for.

- Data from a Normal distribution, looking for changes in the mean, .

- Data from a Normal distribution, looking for changes in the standard deviation .

- Data from a Normal distribution, looking for changes in the mean, and standard deviation .

- Data from a Gamma distribution, looking for changes in the scale parameter .

- Data from an exponential distribution, looking for changes in .

- Data from a Poisson distribution, looking for changes in .

Constraint:

, , , , or .

- 2:

– double array

-

, the time series.

if , that is the data is assumed to come from a Poisson distribution, is used in all calculations.

Constraints:

- if , or , , for ;

- if , each value of y must be representable as an integer;

- if , each value of y must be small enough such that , for , can be calculated without incurring overflow.

Optional Input Parameters

- 1:

– int64int32nag_int scalar

-

Default:

the dimension of the array

y.

, the length of the time series.

Constraint:

.

- 2:

– double scalar

Default:

- if , ;

- otherwise .

, the penalty term.

There are a number of standard ways of setting

, including:

- SIC or BIC

-

- AIC

-

- Hannan-Quinn

-

where

is the number of parameters being treated as estimated in each segment. This is usually set to

when

and

otherwise.

If no penalty is required then set . Generally, the smaller the value of the larger the number of suggested change points.

- 3:

– int64int32nag_int scalar

Default:

The minimum distance between two change points, that is .

Constraint:

.

- 4:

– double array

-

, values for the parameters that will be treated as fixed. If

then

param must be supplied.

- , the standard deviation of the normal distribution. If not supplied then is estimated from the full input data,

- , the mean of the normal distribution. If not supplied then is estimated from the full input data,

- must hold the shape, , for the gamma distribution,

- otherwise

- param is not referenced.

Constraint:

if or , .

Output Parameters

- 1:

– int64int32nag_int array

-

The dimension of the array

tau will be

The location of the change points. The th segment is defined by to , where and .

- 2:

– double array

-

Note: sparam will be an array of size

If , and of size

otherwise.

The estimated values of the distribution parameters in each segment

- , or

-

and

for , where and is the mean and standard deviation, respectively, of the values of in the th segment.

It should be noted that when and when , for all and .

-

and

for , where and are the shape and scale parameters, respectively, for the values of in the th segment. It should be noted that for all .

- or

- for , where is the mean of the values of in the th segment.

- 3:

– int64int32nag_int scalar

unless the function detects an error (see

Error Indicators and Warnings).

Error Indicators and Warnings

Errors or warnings detected by the function:

Cases prefixed with W are classified as warnings and

do not generate an error of type NAG:error_n. See nag_issue_warnings.

-

-

Constraint: , , , , or .

-

-

Constraint: .

-

-

Constraint: if , or then , for .

-

-

On entry, , is too large.

-

-

Constraint: .

-

-

Constraint: if

or

and

param has been supplied, then

.

- W

-

To avoid overflow some truncation occurred when calculating the cost function, . All output is returned as normal.

- W

-

To avoid overflow some truncation occurred when calculating the parameter estimates returned in

sparam. All output is returned as normal.

-

An unexpected error has been triggered by this routine. Please

contact

NAG.

-

Your licence key may have expired or may not have been installed correctly.

-

Dynamic memory allocation failed.

Accuracy

For efficiency reasons, when calculating the cost functions,

and the parameter estimates returned in

sparam, this function makes use of the mathematical identities:

and

where

.

The input data,

, is scaled in order to try and mitigate some of the known instabilities associated with using these formulations. The results returned by

nag_tsa_cp_pelt (g13na) should be sufficient for the majority of datasets. If a more stable method of calculating

is deemed necessary,

nag_tsa_cp_pelt_user (g13nb) can be used and the method chosen implemented in the user-supplied cost function.

Further Comments

None.

Example

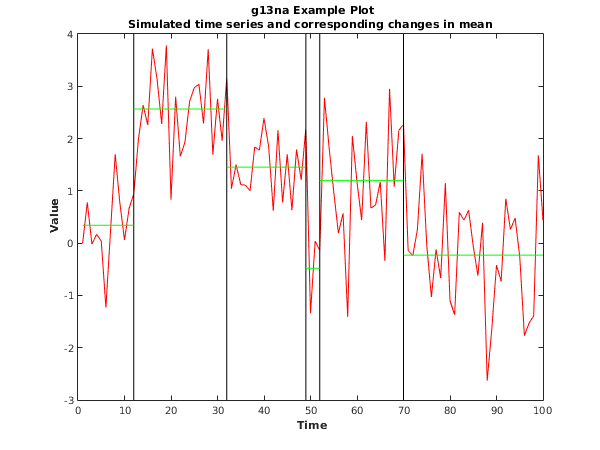

This example identifies changes in the mean, under the assumption that the data is normally distributed, for a simulated dataset with observations. A BIC penalty is used, that is , the minimum segment size is set to and the variance is fixed at across the whole input series.

Open in the MATLAB editor:

g13na_example

function g13na_example

fprintf('g13na example results\n\n');

y = [ 0.00; 0.78;-0.02; 0.17; 0.04;-1.23; 0.24; 1.70; 0.77; 0.06;

0.67; 0.94; 1.99; 2.64; 2.26; 3.72; 3.14; 2.28; 3.78; 0.83;

2.80; 1.66; 1.93; 2.71; 2.97; 3.04; 2.29; 3.71; 1.69; 2.76;

1.96; 3.17; 1.04; 1.50; 1.12; 1.11; 1.00; 1.84; 1.78; 2.39;

1.85; 0.62; 2.16; 0.78; 1.70; 0.63; 1.79; 1.21; 2.20;-1.34;

0.04;-0.14; 2.78; 1.83; 0.98; 0.19; 0.57;-1.41; 2.05; 1.17;

0.44; 2.32; 0.67; 0.73; 1.17;-0.34; 2.95; 1.08; 2.16; 2.27;

-0.14;-0.24; 0.27; 1.71;-0.04;-1.03;-0.12;-0.67; 1.15;-1.10;

-1.37; 0.59; 0.44; 0.63;-0.06;-0.62; 0.39;-2.63;-1.63;-0.42;

-0.73; 0.85; 0.26; 0.48;-0.26;-1.77;-1.53;-1.39; 1.68; 0.43];

ctype = int64(1);

param = 1;

warn_state = nag_issue_warnings();

nag_issue_warnings(true);

[tau,sparam,ifail] = g13na( ...

ctype,y,'param',param);

nag_issue_warnings(warn_state);

fprintf(' -- Change Points -- --- Distribution ---\n');

fprintf(' Number Position Parameters\n');

fprintf(' ==================================================\n');

for i = 1:numel(tau)

fprintf('%5d%13d%16.2f%16.2f\n', i, tau(i), sparam(1:2,i));

end

fig1 = figure;

plot(y,'Color','red');

xpos = transpose(double(tau(1:end-1))*ones(1,2));

ypos = diag(ylim)*ones(2,numel(tau)-1);

line(xpos,ypos,'Color','black');

xpos = transpose(cat(2,cat(1,1,tau(1:end-1)),tau));

ypos = ones(2,1)*sparam(1,:);

line(xpos,ypos,'Color','green');

title({'{\bf g13na Example Plot}',

'Simulated time series and corresponding changes in mean'});

xlabel('{\bf Time}');

ylabel('{\bf Value}');

g13na example results

-- Change Points -- --- Distribution ---

Number Position Parameters

==================================================

1 12 0.34 1.00

2 32 2.57 1.00

3 49 1.45 1.00

4 52 -0.48 1.00

5 70 1.20 1.00

6 100 -0.23 1.00

This example plot shows the original data series, the estimated change points and the estimated mean in each of the identified segments.

PDF version (NAG web site

, 64-bit version, 64-bit version)

© The Numerical Algorithms Group Ltd, Oxford, UK. 2009–2015