PDF version (NAG web site

, 64-bit version, 64-bit version)

NAG Toolbox: nag_pde_1d_blackscholes_closed (d03nd)

Purpose

nag_pde_1d_blackscholes_closed (d03nd) computes an analytic solution to the Black–Scholes equation for a certain set of option types.

Syntax

[

f,

theta,

delta,

gamma,

lambda,

rho,

ifail] = d03nd(

kopt,

x,

s,

t,

tmat,

tdpar,

r,

q,

sigma)

[

f,

theta,

delta,

gamma,

lambda,

rho,

ifail] = nag_pde_1d_blackscholes_closed(

kopt,

x,

s,

t,

tmat,

tdpar,

r,

q,

sigma)

Description

nag_pde_1d_blackscholes_closed (d03nd) computes an analytic solution to the Black–Scholes equation (see

Hull (1989) and

Wilmott et al. (1995))

for the value

of a European put or call option, or an American call option with zero dividend

. In equation

(1) is time,

is the stock price,

is the exercise price,

is the risk free interest rate,

is the continuous dividend, and

is the stock volatility. The parameter

,

and

may be either constant, or functions of time. In the latter case their average instantaneous values over the remaining life of the option should be provided to

nag_pde_1d_blackscholes_closed (d03nd). An auxiliary function

nag_pde_1d_blackscholes_means (d03ne) is available to compute such averages from values at a set of discrete times. Equation

(1) is subject to different boundary conditions depending on the type of option. For a call option the boundary condition is

where

is the maturity time of the option. For a put option the equation

(1) is subject to

nag_pde_1d_blackscholes_closed (d03nd) also returns values of the Greeks

nag_specfun_opt_bsm_greeks (s30ab) also computes the European option price given by the Black–Scholes–Merton formula together with a more comprehensive set of sensitivities (Greeks).

Further details of the analytic solution returned are given in

Algorithmic Details.

References

Hull J (1989) Options, Futures and Other Derivative Securities Prentice–Hall

Wilmott P, Howison S and Dewynne J (1995) The Mathematics of Financial Derivatives Cambridge University Press

Parameters

Compulsory Input Parameters

- 1:

– int64int32nag_int scalar

-

Specifies the kind of option to be valued:

- A European call option.

- An American call option.

- A European put option.

Constraints:

- , or ;

- if , .

- 2:

– double scalar

-

The exercise price .

Constraint:

.

- 3:

– double scalar

-

The stock price at which the option value and the Greeks should be evaluated.

Constraint:

.

- 4:

– double scalar

-

The time at which the option value and the Greeks should be evaluated.

Constraint:

.

- 5:

– double scalar

-

The maturity time of the option.

Constraint:

.

- 6:

– logical array

-

Specifies whether or not various arguments are time-dependent. More precisely, is time-dependent if and constant otherwise. Similarly, specifies whether is time-dependent and specifies whether is time-dependent.

- 7:

– double array

-

The dimension of the array

r

must be at least

if

, and at least

otherwise

If

then

must contain the constant value of

. The remaining elements need not be set.

If

then

must contain the value of

at time

t and

must contain its average instantaneous value over the remaining life of the option:

The auxiliary function

nag_pde_1d_blackscholes_means (d03ne) may be used to construct

r from a set of values of

at discrete times.

- 8:

– double array

-

The dimension of the array

q

must be at least

if

, and at least

otherwise

If

then

must contain the constant value of

. The remaining elements need not be set.

If

then

must contain the constant value of

and

must contain its average instantaneous value over the remaining life of the option:

The auxiliary function

nag_pde_1d_blackscholes_means (d03ne) may be used to construct

q from a set of values of

at discrete times.

- 9:

– double array

-

The dimension of the array

sigma

must be at least

if

, and at least

otherwise

If

then

must contain the constant value of

. The remaining elements need not be set.

If

then

must contain the value of

at time

t,

the average instantaneous value

, and

the second-order average

, where:

The auxiliary function

nag_pde_1d_blackscholes_means (d03ne) may be used to compute

sigma from a set of values at discrete times.

Constraints:

- if , ;

- if , , for .

Optional Input Parameters

None.

Output Parameters

- 1:

– double scalar

-

The value

of the option at the stock price

s and time

t.

- 2:

– double scalar

- 3:

– double scalar

- 4:

– double scalar

- 5:

– double scalar

- 6:

– double scalar

-

The values of various Greeks at the stock price

s and time

t, as follows:

- 7:

– int64int32nag_int scalar

unless the function detects an error (see

Error Indicators and Warnings).

Error Indicators and Warnings

Errors or warnings detected by the function:

-

-

| On entry, | , |

| or | , |

| or | when , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , with , |

| or | , with , for some , or . |

-

An unexpected error has been triggered by this routine. Please

contact

NAG.

-

Your licence key may have expired or may not have been installed correctly.

-

Dynamic memory allocation failed.

Accuracy

Given accurate values of

r,

q and

sigma no further approximations are made in the evaluation of the Black–Scholes analytic formulae, and the results should therefore be within machine accuracy. The values of

r,

q and

sigma returned from

nag_pde_1d_blackscholes_means (d03ne) are exact for polynomials of degree up to

.

Further Comments

Algorithmic Details

The Black–Scholes analytic formulae are used to compute the solution. For a European call option these are as follows:

where

is the cumulative Normal distribution function and

is its derivative

The functions

,

,

and

are average values of

,

and

over the time to maturity:

The Greeks are then calculated as follows:

Note: that is obtained from substitution of other Greeks in the Black–Scholes partial differential equation, rather than differentiation of . The values of , and appearing in its definition are the instantaneous values, not the averages. Note also that both the first-order average and the second-order average appear in the expression for . This results from the fact that is the derivative of with respect to , not .

For a European put option the equivalent equations are:

The analytic solution for an American call option with is identical to that for a European call, since early exercise is never optimal in this case. For all other cases no analytic solution is known.

Example

This example solves the Black–Scholes equation for valuation of a -month American call option on a non-dividend-paying stock with an exercise price of $50. The risk-free interest rate is 10% per annum, and the stock volatility is 40% per annum.

The option is valued at a range of times and stock prices.

Open in the MATLAB editor:

d03nd_example

function d03nd_example

fprintf('d03nd example results\n\n');

kopt = int64(2);

x = 50;

ns = 21; nt = 4;

s_beg = 0; t_beg = 0;

s_end = 100; t_end = 0.125;

tmat = 0.4166667;

tdpar = [false; false; false];

r = [0.1];

q = [0];

sigma = [0.4];

ds = (s_end-s_beg)/(ns-1);

dt = (t_end-t_beg)/(nt-1);

s = [s_beg:ds:s_end];

t = [t_beg:dt:t_end];

f = zeros(ns,nt);

theta = f; delta = f; gamma = f; lambda = f; rho = f;

for j = 1:nt

for i = 1:ns

[f(i,j),theta(i,j),delta(i,j),gamma(i,j),lambda(i,j),rho(i,j),ifail] = ...

d03nd( ...

kopt, x, s(i), t(j), tmat, tdpar, r, q, sigma);

end

end

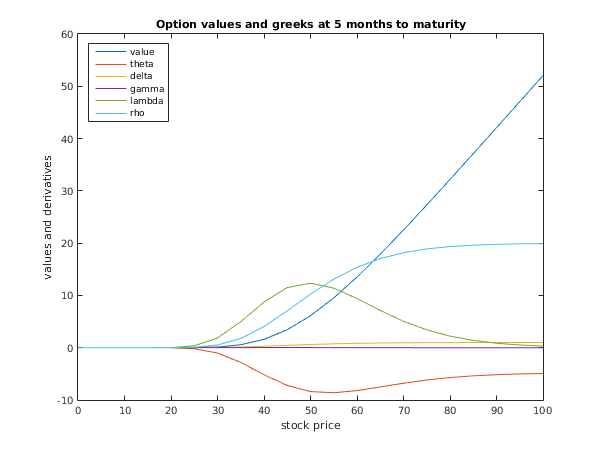

print_greek(ns,nt,tmat,s,t,'Option Values',f);

fig1 = figure;

plot(s,f(:,1),s,theta(:,1),s,delta(:,1),s,gamma(:,1),s,lambda(:,1),s,rho(:,1));

legend('value','theta','delta','gamma','lambda','rho','Location','NorthWest');

title('Option values and greeks at 5 months to maturity');

xlabel('stock price');

ylabel('values and derivatives');

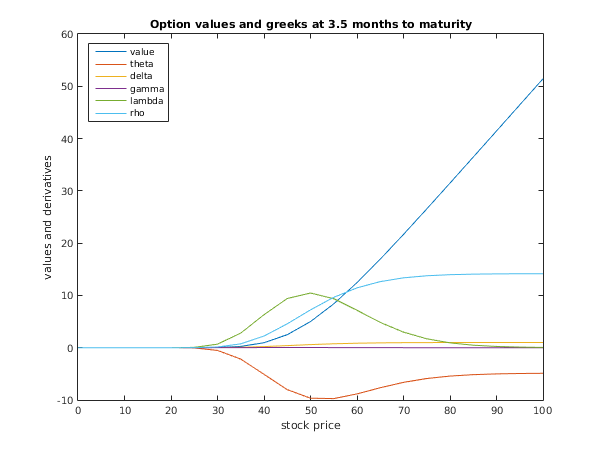

fig2 = figure;

plot(s,f(:,4),s,theta(:,4),s,delta(:,4),s,gamma(:,4),s,lambda(:,4),s,rho(:,4));

legend('value','theta','delta','gamma','lambda','rho','Location','NorthWest');

title('Option values and greeks at 3.5 months to maturity');

xlabel('stock price');

ylabel('values and derivatives');

function print_greek(ns,nt,tmat,s,t,grname,greek)

fprintf('\n%s\n\n',grname);

fprintf(' Stock Price | Time to Maturity (months)\n');

fprintf('%16s %12.4e%12.4e%12.4e%12.4e\n', '|', 12*(tmat-t));

fprintf('%15s+%48s\n', '---------------', ...

'-------------------------------------------------');

for i = 1:ns

fprintf('%12.4e%4s %12.4e%12.4e%12.4e%12.4e\n', s(i), '|', greek(i,:));

end

d03nd example results

Option Values

Stock Price | Time to Maturity (months)

| 5.0000e+00 4.5000e+00 4.0000e+00 3.5000e+00

---------------+-------------------------------------------------

0.0000e+00 | 0.0000e+00 0.0000e+00 0.0000e+00 0.0000e+00

5.0000e+00 | 4.4491e-19 4.5989e-21 1.5461e-23 1.0478e-26

1.0000e+01 | 5.5566e-10 5.5129e-11 3.1298e-12 8.0281e-14

1.5000e+01 | 4.7337e-06 1.2187e-06 2.2774e-07 2.7003e-08

2.0000e+01 | 7.2236e-04 3.1054e-04 1.1005e-04 2.9678e-05

2.5000e+01 | 1.6557e-02 9.6610e-03 5.0099e-03 2.2012e-03

3.0000e+01 | 1.3307e-01 9.4037e-02 6.1869e-02 3.6848e-02

3.5000e+01 | 5.6631e-01 4.5257e-01 3.4667e-01 2.5053e-01

4.0000e+01 | 1.6004e+00 1.3850e+00 1.1699e+00 9.5640e-01

4.5000e+01 | 3.4384e+00 3.1328e+00 2.8168e+00 2.4891e+00

5.0000e+01 | 6.1165e+00 5.7600e+00 5.3874e+00 4.9960e+00

5.5000e+01 | 9.5300e+00 9.1645e+00 8.7846e+00 8.3882e+00

6.0000e+01 | 1.3509e+01 1.3163e+01 1.2808e+01 1.2445e+01

6.5000e+01 | 1.7883e+01 1.7568e+01 1.7251e+01 1.6932e+01

7.0000e+01 | 2.2513e+01 2.2230e+01 2.1949e+01 2.1671e+01

7.5000e+01 | 2.7301e+01 2.7045e+01 2.6792e+01 2.6544e+01

8.0000e+01 | 3.2182e+01 3.1946e+01 3.1713e+01 3.1485e+01

8.5000e+01 | 3.7117e+01 3.6894e+01 3.6674e+01 3.6458e+01

9.0000e+01 | 4.2081e+01 4.1868e+01 4.1656e+01 4.1446e+01

9.5000e+01 | 4.7062e+01 4.6854e+01 4.6647e+01 4.6441e+01

1.0000e+02 | 5.2052e+01 5.1847e+01 5.1643e+01 5.1439e+01

PDF version (NAG web site

, 64-bit version, 64-bit version)

© The Numerical Algorithms Group Ltd, Oxford, UK. 2009–2015