PDF version (NAG web site

, 64-bit version, 64-bit version)

NAG Toolbox: nag_mv_prin_comp (g03aa)

Purpose

nag_mv_prin_comp (g03aa) performs a principal component analysis on a data matrix; both the principal component loadings and the principal component scores are returned.

Syntax

[

s,

e,

p,

v,

ifail] = g03aa(

matrix,

std,

x,

isx,

s,

nvar, 'n',

n, 'm',

m, 'wt',

wt)

[

s,

e,

p,

v,

ifail] = nag_mv_prin_comp(

matrix,

std,

x,

isx,

s,

nvar, 'n',

n, 'm',

m, 'wt',

wt)

Note: the interface to this routine has changed since earlier releases of the toolbox:

| At Mark 24: |

weight was removed from the interface; wt was made optional |

| At Mark 22: |

n was made optional |

Description

Let

be an

by

data matrix of

observations on

variables

and let the

by

variance-covariance matrix of

be

. A vector

of length

is found such that:

The variable

is known as the first principal component and gives the linear combination of the variables that gives the maximum variation. A second principal component,

, is found such that:

This gives the linear combination of variables that is orthogonal to the first principal component that gives the maximum variation. Further principal components are derived in a similar way.

The vectors

, are the eigenvectors of the matrix

and associated with each eigenvector is the eigenvalue,

. The value of

gives the proportion of variation explained by the

th principal component. Alternatively, the

's can be considered as the right singular vectors in a singular value decomposition with singular values

of the data matrix centred about its mean and scaled by

,

. This latter approach is used in

nag_mv_prin_comp (g03aa), with

where

is a diagonal matrix with elements

,

is the

by

matrix with columns

and

is an

by

matrix with

, which gives the principal component scores.

Principal component analysis is often used to reduce the dimension of a dataset, replacing a large number of correlated variables with a smaller number of orthogonal variables that still contain most of the information in the original dataset.

The choice of the number of dimensions required is usually based on the amount of variation accounted for by the leading principal components. If

principal components are selected, then a test of the equality of the remaining

eigenvalues is

which has, asymptotically, a

-distribution with

degrees of freedom.

Equality of the remaining eigenvalues indicates that if any more principal components are to be considered then they all should be considered.

Instead of the variance-covariance matrix the correlation matrix, the sums of squares and cross-products matrix or a standardized sums of squares and cross-products matrix may be used. In the last case is replaced by for a diagonal matrix with positive elements. If the correlation matrix is used, the approximation for the statistic given above is not valid.

The principal component scores, , are the values of the principal component variables for the observations. These can be standardized so that the variance of these scores for each principal component is or equal to the corresponding eigenvalue.

Weights can be used with the analysis, in which case the matrix is first centred about the weighted means then each row is scaled by an amount , where is the weight for the th observation.

References

Chatfield C and Collins A J (1980) Introduction to Multivariate Analysis Chapman and Hall

Cooley W C and Lohnes P R (1971) Multivariate Data Analysis Wiley

Hammarling S (1985) The singular value decomposition in multivariate statistics SIGNUM Newsl. 20(3) 2–25

Kendall M G and Stuart A (1969) The Advanced Theory of Statistics (Volume 1) (3rd Edition) Griffin

Morrison D F (1967) Multivariate Statistical Methods McGraw–Hill

Parameters

Compulsory Input Parameters

- 1:

– string (length ≥ 1)

-

Indicates for which type of matrix the principal component analysis is to be carried out.

- It is for the correlation matrix.

- It is for a standardized matrix, with standardizations given by s.

- It is for the sums of squares and cross-products matrix.

- It is for the variance-covariance matrix.

Constraint:

, , or .

- 2:

– string (length ≥ 1)

-

Indicates if the principal component scores are to be standardized.

- The principal component scores are standardized so that , i.e., .

- The principal component scores are unstandardized, i.e., .

- The principal component scores are standardized so that they have unit variance.

- The principal component scores are standardized so that they have variance equal to the corresponding eigenvalue.

Constraint:

, , or .

- 3:

– double array

-

ldx, the first dimension of the array, must satisfy the constraint

.

must contain the th observation for the th variable, for and .

- 4:

– int64int32nag_int array

-

indicates whether or not the

th variable is to be included in the analysis.

If

, the variable contained in the

th column of

x is included in the principal component analysis, for

.

Constraint:

for

nvar values of

.

- 5:

– double array

-

The standardizations to be used, if any.

If

, the first

elements of

s must contain the standardization coefficients, the diagonal elements of

.

Constraint:

if , , for .

- 6:

– int64int32nag_int scalar

-

, the number of variables in the principal component analysis.

Constraint:

.

Optional Input Parameters

- 1:

– int64int32nag_int scalar

-

Default:

the first dimension of the array

x.

, the number of observations.

Constraint:

.

- 2:

– int64int32nag_int scalar

-

Default:

the dimension of the arrays

isx,

s and the second dimension of the array

x. (An error is raised if these dimensions are not equal.)

, the number of variables in the data matrix.

Constraint:

.

- 3:

– double array

-

The dimension of the array

wt

must be at least

if

, and at least

otherwise

If

, the first

elements of

wt must contain the weights to be used in the principal component analysis.

If , the th observation is not included in the analysis. The effective number of observations is the sum of the weights.

If

,

wt is not referenced and the effective number of observations is

.

Constraints:

- , for ;

- the sum of weights .

Output Parameters

- 1:

– double array

-

If

,

s is unchanged on exit.

If

,

s contains the variances of the selected variables.

contains the variance of the variable in the

th column of

x if

.

If

or

,

s is not referenced.

- 2:

– double array

-

The statistics of the principal component analysis.

- The eigenvalues associated with the

th principal component, , for .

- The proportion of variation explained by the

th principal component, for .

- The cumulative proportion of variation explained by the first

th principal components, for .

- The statistics, for .

- The degrees of freedom for the statistics, for .

If ,

contains significance level for the statistic, for .

If , is returned as zero.

- 3:

– double array

-

The first

nvar columns of

p contain the principal component loadings,

. The

th column of

p contains the

nvar coefficients for the

th principal component.

- 4:

– double array

-

The first

nvar columns of

v contain the principal component scores. The

th column of

v contains the

n scores for the

th principal component.

If , any rows for which is zero will be set to zero.

- 5:

– int64int32nag_int scalar

unless the function detects an error (see

Error Indicators and Warnings).

Error Indicators and Warnings

Errors or warnings detected by the function:

Cases prefixed with W are classified as warnings and

do not generate an error of type NAG:error_n. See nag_issue_warnings.

-

-

| On entry, | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , , or , |

| or | , , or , |

| or | or . |

-

-

| On entry, | and a value of . |

-

-

| On entry, | there are not nvar values of , |

| or | and the effective number of observations is less than . |

-

-

| On entry, | for some , when and . |

-

-

The singular value decomposition has failed to converge. This is an unlikely error exit.

- W

-

All eigenvalues/singular values are zero. This will be caused by all the variables being constant.

-

An unexpected error has been triggered by this routine. Please

contact

NAG.

-

Your licence key may have expired or may not have been installed correctly.

-

Dynamic memory allocation failed.

Accuracy

As nag_mv_prin_comp (g03aa) uses a singular value decomposition of the data matrix, it will be less affected by ill-conditioned problems than traditional methods using the eigenvalue decomposition of the variance-covariance matrix.

Further Comments

None.

Example

A dataset is taken from

Cooley and Lohnes (1971), it consists of ten observations on three variables. The unweighted principal components based on the variance-covariance matrix are computed and the principal component scores requested. The principal component scores are standardized so that they have variance equal to the corresponding eigenvalue.

Open in the MATLAB editor:

g03aa_example

function g03aa_example

fprintf('g03aa example results\n\n');

x = [7, 4, 3;

4, 1, 8;

6, 3, 5;

8, 6, 1;

8, 5, 7;

7, 2, 9;

5, 3, 3;

9, 5, 8;

7, 4, 5;

8, 2, 2];

n = size(x,2);

matrix = 'V';

std = 'E';

isx = ones(n,1,'int64');

s = zeros(n,1);

nvar = int64(n);

[s, e, p, v, ifail] = g03aa( ...

matrix, std, x, isx, s, nvar);

fprintf('Eigenvalues Percentage Cumulative Chisq DF Sig\n');

fprintf(' variation variation\n\n');

fprintf('%11.4f%12.4f%12.4f%10.4f%8.1f%8.4f\n',e');

fprintf('\n');

mtitle = 'Principal component loadings';

matrix = 'General';

diag = ' ';

[ifail] = x04ca( ...

matrix, diag, p, mtitle);

fprintf('\n');

mtitle = 'Principal component scores';

[ifail] = x04ca( ...

matrix, diag, v, mtitle);

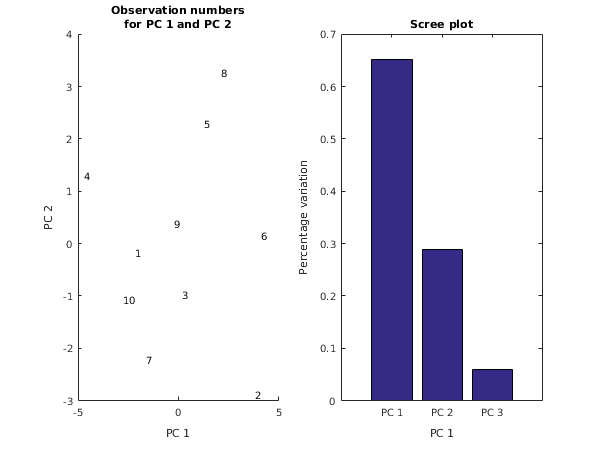

fig1 = figure;

subplot(1,2,1);

xlabel('PC 1');

ylabel('PC 2');

title({'Observation numbers', 'for PC 1 and PC 2'});

axis([-5 5 -3 4]);

for j = 1:size(x,1)

ch = sprintf('%d',j);

text(v(j,1),v(j,2),ch);

end

subplot(1,2,2);

bar(e(:,2));

ax = gca;

ax.XTickLabel = {'PC 1','PC 2','PC 3'};

xlabel('PC 1');

ylabel('Percentage variation');

title('Scree plot');

g03aa example results

Eigenvalues Percentage Cumulative Chisq DF Sig

variation variation

8.2739 0.6515 0.6515 8.6127 5.0 0.1255

3.6761 0.2895 0.9410 4.1183 2.0 0.1276

0.7499 0.0590 1.0000 0.0000 0.0 0.0000

Principal component loadings

1 2 3

1 -0.1376 0.6990 -0.7017

2 -0.2505 0.6609 0.7075

3 0.9583 0.2731 0.0842

Principal component scores

1 2 3

1 -2.1514 -0.1731 0.1068

2 3.8042 -2.8875 0.5104

3 0.1532 -0.9869 0.2694

4 -4.7065 1.3015 0.6517

5 1.2938 2.2791 0.4492

6 4.0993 0.1436 -0.8031

7 -1.6258 -2.2321 0.8028

8 2.1145 3.2512 -0.1684

9 -0.2348 0.3730 0.2751

10 -2.7464 -1.0689 -2.0940

PDF version (NAG web site

, 64-bit version, 64-bit version)

© The Numerical Algorithms Group Ltd, Oxford, UK. 2009–2015