PDF version (NAG web site

, 64-bit version, 64-bit version)

NAG Toolbox: nag_pde_1d_blackscholes_fd (d03nc)

Purpose

nag_pde_1d_blackscholes_fd (d03nc) solves the Black–Scholes equation for financial option pricing using a finite difference scheme.

Syntax

[

s,

t,

f,

theta,

delta,

gamma,

lambda,

rho,

ifail] = d03nc(

kopt,

x,

mesh,

s,

t,

tdpar,

r,

q,

sigma,

ntkeep, 'ns',

ns, 'nt',

nt, 'alpha',

alpha)

[

s,

t,

f,

theta,

delta,

gamma,

lambda,

rho,

ifail] = nag_pde_1d_blackscholes_fd(

kopt,

x,

mesh,

s,

t,

tdpar,

r,

q,

sigma,

ntkeep, 'ns',

ns, 'nt',

nt, 'alpha',

alpha)

Description

nag_pde_1d_blackscholes_fd (d03nc) solves the Black–Scholes equation (see

Hull (1989) and

Wilmott et al. (1995))

for the value

of a European or American, put or call stock option, with exercise price

. In equation

(1) is time,

is the stock price,

is the risk free interest rate,

is the continuous dividend, and

is the stock volatility. According to the values in the array

tdpar, the arguments

,

and

may each be either constant or functions of time. The function also returns values of various Greeks.

nag_pde_1d_blackscholes_fd (d03nc) uses a finite difference method with a choice of time-stepping schemes. The method is explicit for

and implicit for nonzero values of

alpha. Second order time accuracy can be obtained by setting

. According to the value of the argument

mesh the finite difference mesh may be either uniform, or user-defined in both

and

directions.

References

Hull J (1989) Options, Futures and Other Derivative Securities Prentice–Hall

Wilmott P, Howison S and Dewynne J (1995) The Mathematics of Financial Derivatives Cambridge University Press

Parameters

Compulsory Input Parameters

- 1:

– int64int32nag_int scalar

-

Specifies the kind of option to be valued.

- A European call option.

- An American call option.

- A European put option.

- An American put option.

Constraint:

, , or .

- 2:

– double scalar

-

The exercise price .

- 3:

– string (length ≥ 1)

-

Indicates the type of finite difference mesh to be used:

- Uniform mesh.

- Custom mesh supplied by you.

Constraint:

or .

- 4:

– double array

-

If

,

must contain the

th stock price in the mesh, for

. These values should be in increasing order, with

and

.

If , must be set to and to , but need not be initialized, as they will be set internally by the function in order to define a uniform mesh.

Constraints:

- if , and , for ;

- if , .

- 5:

– double array

-

If

then

must contain the

th time in the mesh, for

. These values should be in increasing order, with

and

.

If then must be set to and to , but need not be initialized, as they will be set internally by the function in order to define a uniform mesh.

Constraints:

- if , and , for ;

- if , .

- 6:

– logical array

-

Specifies whether or not various arguments are time-dependent. More precisely, is time-dependent if and constant otherwise. Similarly, specifies whether is time-dependent and specifies whether is time-dependent.

- 7:

– double array

-

The dimension of the array

r

must be at least

if

, and at least

otherwise

If

then

must contain the value of the risk-free interest rate

at the

th time in the mesh, for

.

If then must contain the constant value of the risk-free interest rate . The remaining elements need not be set.

- 8:

– double array

-

The dimension of the array

q

must be at least

if

, and at least

otherwise

If

then

must contain the value of the continuous dividend

at the

th time in the mesh, for

.

If then must contain the constant value of the continuous dividend . The remaining elements need not be set.

- 9:

– double array

-

The dimension of the array

sigma

must be at least

if

, and at least

otherwise

If

then

must contain the value of the volatility

at the

th time in the mesh, for

.

If then must contain the constant value of the volatility . The remaining elements need not be set.

- 10:

– int64int32nag_int scalar

-

The number of solutions to be stored in the time direction. The function calculates the solution backwards from

to

at all times in the mesh. These time solutions and the corresponding Greeks will be stored at times

, for

, in the arrays

f,

theta,

delta,

gamma,

lambda and

rho. Other time solutions will be discarded. To store all time solutions set

.

Constraint:

.

Optional Input Parameters

- 1:

– int64int32nag_int scalar

-

Default:

the dimension of the array

s.

The number of stock prices to be used in the finite difference mesh.

Constraint:

.

- 2:

– int64int32nag_int scalar

-

Default:

the dimension of the array

t.

The number of time-steps to be used in the finite difference method.

Constraint:

.

- 3:

– double scalar

Default:

The value of

to be used in the time-stepping scheme. Typical values include:

- Explicit forward Euler scheme.

- Implicit Crank–Nicolson scheme.

- Implicit backward Euler scheme.

The value gives second-order accuracy in time. Values greater than give unconditional stability. Since is at the limit of unconditional stability this value does not damp oscillations.

Constraint:

.

Output Parameters

- 1:

– double array

-

If

, the elements of

s define a uniform mesh over

.

If

, the elements of

s are unchanged.

- 2:

– double array

-

If

, the elements of

t define a uniform mesh over

.

If

, the elements of

t are unchanged.

- 3:

– double array

-

, for and , contains the value of the option at the th mesh point at time .

- 4:

– double array

- 5:

– double array

- 6:

– double array

- 7:

– double array

- 8:

– double array

-

The values of various Greeks at the

th mesh point

at time

, as follows:

- 9:

– int64int32nag_int scalar

unless the function detects an error (see

Error Indicators and Warnings).

Error Indicators and Warnings

Errors or warnings detected by the function:

-

-

| On entry, | , |

| or | , |

| or | or , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | , |

| or | . |

-

-

and the constraints:

are violated. Thus the end points of the uniform mesh are not in order.

-

-

and the constraints:

- , for ,

- , for

are violated. Thus the mesh points are not in order.

-

An unexpected error has been triggered by this routine. Please

contact

NAG.

-

Your licence key may have expired or may not have been installed correctly.

-

Dynamic memory allocation failed.

Accuracy

The accuracy of the solution

and the various derivatives returned by the function is dependent on the values of

ns and

nt supplied, the distribution of the mesh points, and the value of

alpha chosen. For most choices of

alpha the solution has a truncation error which is second-order accurate in

and first order accurate in

. For

the truncation error is also second-order accurate in

.

The simplest approach to improving the accuracy is to increase the values of both

ns and

nt.

Further Comments

Timing

Each time-step requires the construction and solution of a tridiagonal system of linear equations. To calculate each of the derivatives

lambda and

rho requires a repetition of the entire solution process. The time taken for a call to the function is therefore proportional to

.

Algorithmic Details

nag_pde_1d_blackscholes_fd (d03nc) solves equation

(1) using a finite difference method. The solution is computed backwards in time from

to

using a

scheme, which is implicit for all nonzero values of

, and is unconditionally stable for values of

. For each time-step a tridiagonal system is constructed and solved to obtain the solution at the earlier time. For the explicit scheme (

) this tridiagonal system degenerates to a diagonal matrix and is solved trivially. For American options the solution at each time-step is inspected to check whether early exercise is beneficial, and amended accordingly.

To compute the arrays

lambda and

rho, which are derivatives of the stock value

with respect to the problem arguments

and

respectively, the entire solution process is repeated with perturbed values of these arguments.

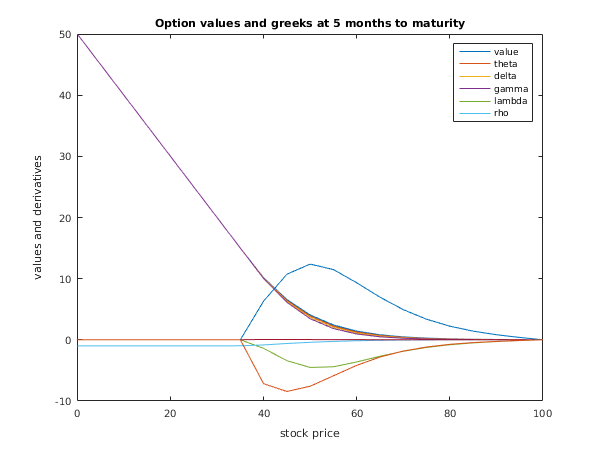

Example

This example, taken from

Hull (1989), solves the one-dimensional Black–Scholes equation for valuation of a

-month American put option on a non-dividend-paying stock with an exercise price of $50. The risk-free interest rate is 10% per annum, and the stock volatility is 40% per annum.

A fully implicit backward Euler scheme is used, with a mesh of stock price intervals and time intervals.

Open in the MATLAB editor:

d03nc_example

function d03nc_example

fprintf('d03nc example results\n\n');

kopt = int64(4);

x = 50;

mesh = 'U';

n = 21;

nt = 11;

s = zeros(n,1);

s(n) = 100;

t = zeros(nt,1);

t(nt) = 0.4166667;

tdpar = [false; false; false];

r = [0.1];

q = [0];

sigma = [0.4];

ntkeep = int64(4);

alpha = 1;

[s, t, f, theta, delta, gamma, lambda, rho, ifail] = ...

d03nc(...

kopt, x, mesh, s, t, tdpar, r, q, sigma, ntkeep,'alpha',alpha);

disp(' Option Values');

disp(' Stock Price | Time to Maturity (months)');

fprintf('%16s','|');

fprintf('%12.1f',12*(t(nt)-t(1:ntkeep)));

fprintf('\n');

for i = 1:n

fprintf('%12.0f%4s', s(i), '|');

fprintf(' %12.5f', f(i,:));

fprintf('\n');

end

fig1 = figure;

plot(s,f,s,theta(:,1),s,delta(:,1),s,gamma(:,1),s,...

lambda(:,1),s,rho(:,1));

legend('value','theta','delta','gamma','lambda','rho');

title('Option values and greeks at 5 months to maturity');

xlabel('stock price');

ylabel('values and derivatives');

d03nc example results

Option Values

Stock Price | Time to Maturity (months)

| 5.0 4.5 4.0 3.5

0 | 50.00000 50.00000 50.00000 50.00000

5 | 45.00000 45.00000 45.00000 45.00000

10 | 40.00000 40.00000 40.00000 40.00000

15 | 35.00000 35.00000 35.00000 35.00000

20 | 30.00000 30.00000 30.00000 30.00000

25 | 25.00000 25.00000 25.00000 25.00000

30 | 20.00000 20.00000 20.00000 20.00000

35 | 15.00000 15.00000 15.00000 15.00000

40 | 10.15432 10.09580 10.04640 10.01169

45 | 6.58481 6.44237 6.29161 6.13058

50 | 4.06719 3.87850 3.67292 3.44630

55 | 2.42637 2.24235 2.04536 1.83361

60 | 1.41742 1.26619 1.10958 0.94813

65 | 0.81951 0.70724 0.59532 0.48515

70 | 0.47241 0.39411 0.31904 0.24845

75 | 0.27257 0.22016 0.17174 0.12815

80 | 0.15725 0.12328 0.09294 0.06668

85 | 0.08966 0.06848 0.05010 0.03473

90 | 0.04845 0.03625 0.02590 0.01747

95 | 0.02110 0.01558 0.01097 0.00727

100 | 0.00000 0.00000 0.00000 0.00000

PDF version (NAG web site

, 64-bit version, 64-bit version)

© The Numerical Algorithms Group Ltd, Oxford, UK. 2009–2015